Cross-border Payments: Wires vs Stablecoins

Optimizing Wire Transfers and Stablecoins across High, Medium, and Low-Liquidity Cross-Border Corridors

Building on my previous posts around stablecoins and infrastructure modernization, this article explores how cross-border orchestrators can shift from viewing stablecoins as wire transfer replacements to treating them as complementary optimization tools.

This framework identifies three deployment scenarios: high-liquidity corridors (USD-EUR, USD-GBP) where stablecoins excel for speed-sensitive segments, medium-liquidity markets (USD-MXN, USD-BRL) requiring hybrid strategies, and low-liquidity emerging markets maintaining wire-first approaches.

Cross-border orchestration

Cross-border payments represent one of the most compelling use cases where stablecoins can serve as an answer to mitigating forex volatility risk and lowering transfer costs. While the debate continues on whether stablecoins will replace wire transfers, smart orchestrators are asking a different question: How do we optimize both?

The answer may not lie in choosing between traditional and digital rails, but rather in strategically deploying each where they excel. That is exactly the path some of the larger players are taking now. JP Morgan's JPM Coin processes over $1 billion daily alongside traditional correspondent banking. Visa's settlement network combines traditional rails with blockchain infrastructure. These aren't replacement strategies—they are complementary optimization plays.

While wires remain a tried and tested route for cross-border payments, stablecoins, although showing strong potential, carry significant unknowns around compliance, coverage, and technology risk. So, in addition to understanding exactly when stablecoins deliver superior value, orchestrators need to weigh these factors when planning transaction routing and build systematic approaches to capture both customer value and revenue margins.

Understanding the Value Chain

To evaluate stablecoins against wires (traditional) rails, we first need to understand the workflow for each of these rails. The economics are fundamentally different, not just cheaper or more expensive.

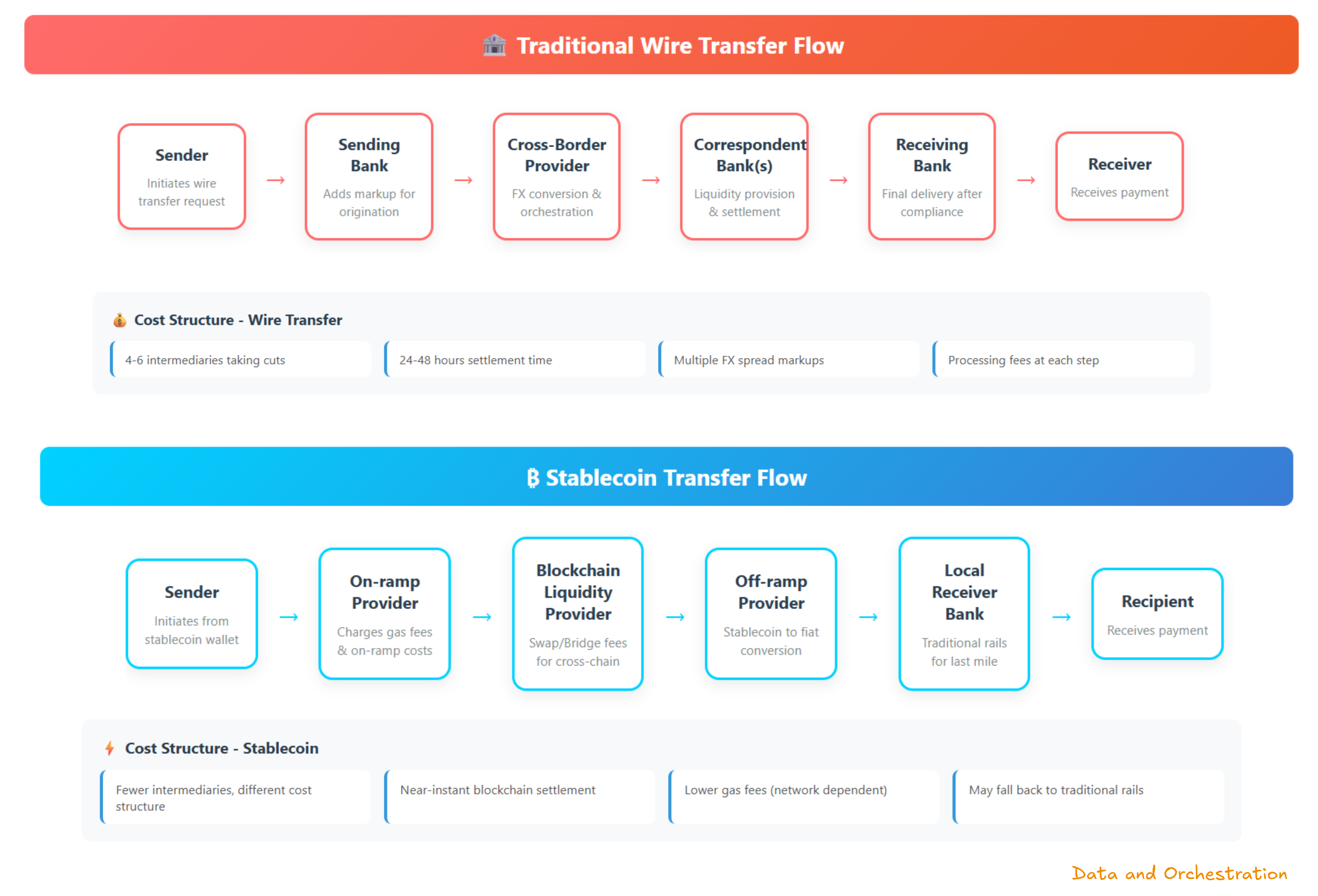

Wire SWIFT Flow (Traditional Rails)

Whether for gig worker payouts where Uber, Lyft, DoorDash send daily/weekly earnings to drivers in foreign domiciles or large-value cross-border payments for interbank settlements, corporate trade finance or supply chain payments wire transactions have often been the main mode of money movement.

A typical $10,000 wire transfer moves through 4-6 intermediaries over 24-48 hours with multiple intermediaries taking a cut of the forex spread and extracting processing fees.

Sender → Sending Bank → Cross-Border Provider → Correspondent Bank(s) → Receiving Bank → ReceiverSender (typically an institution) initiates a wire transfer.

Sending Bank adds a markup for origination

Cross-Border Provider solutions orchestration and FX conversion

Correspondent Bank(s) owns the last mile payout, ensures liquidity provision and settlement

Receiving Bank is responsible for final delivery to the receiver after compliance checks.

Stablecoin Flow

Sender → On-ramp providers → Blockchain liquidity providers → Off-ramp providers → Local Receiver Bank → RecipientThe same $10,000 transaction through stablecoins can involve fewer intermediaries but different cost structures.

Sender initiates a cross-border payment from his stablecoin wallet.

Stablecoin provider charges a fee to cover the operational costs such as gas fees to get the money on-ramp (smart contract on blockchain)

Stablecoin liquidity providers help move money across the blockchain and take a cut in terms of fee for Swap/Bridge. For example - if USDC is the originating stablecoin and the receiving market is primarily USDT, swap may be needed.

Off-ramp provider takes care of the stablecoin to fiat conversion in the receive currency.

Local Payout In situations where the conversion or payout cannot directly happen to the recipient’s bank account the last mile payout can switch to traditional rails with forex spread.

Liquidity and adoption of Stablecoins matter

The economics of stablecoins are heavily dependent on three factors:

Adoption in the originating market

Liquidity in the receiving market

Adoption in the receiving market

Of these three, liquidity and adoption in the receiving market can be major factors in deciding whether stablecoin payouts make sense.

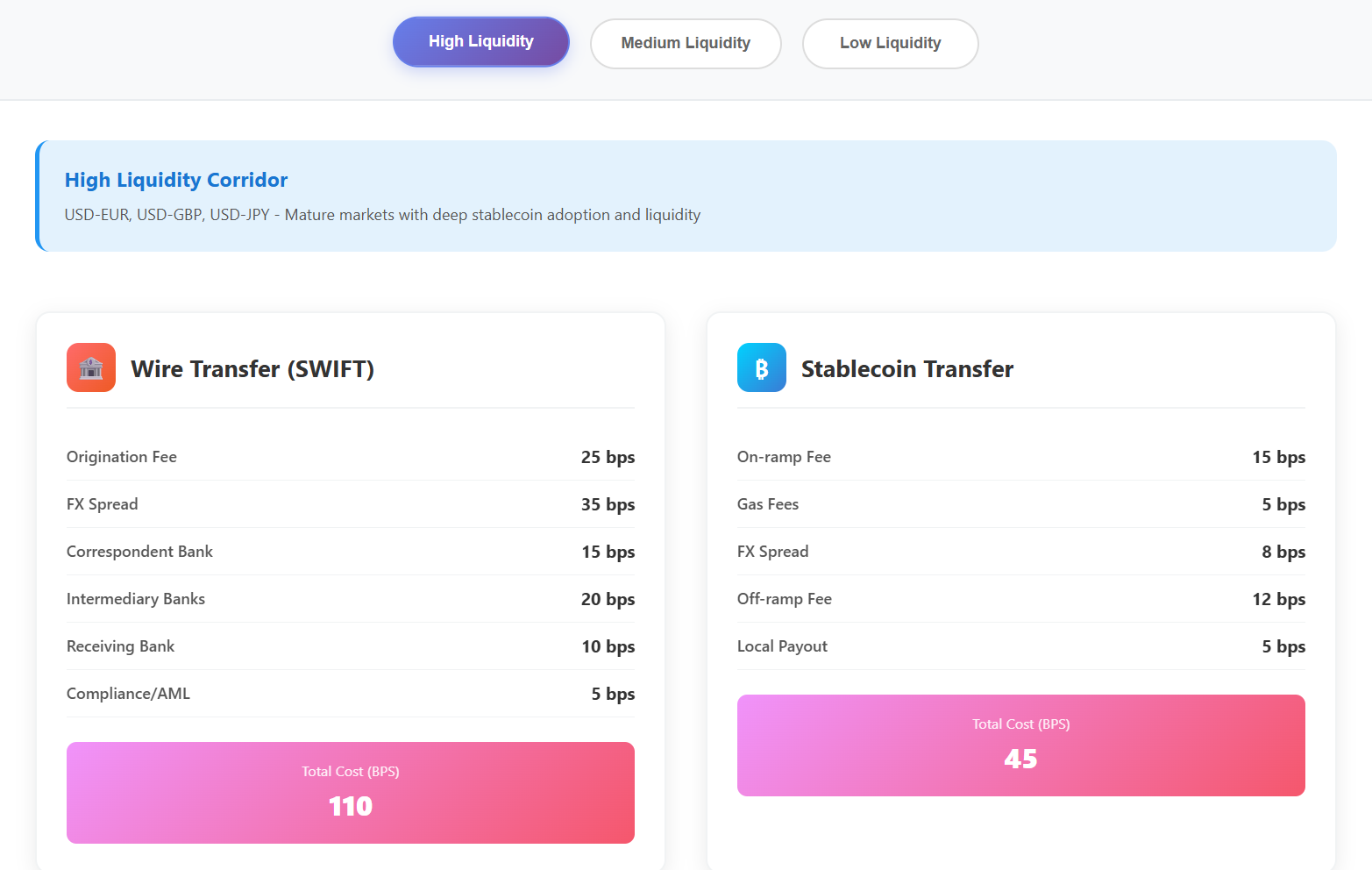

Bps Analysis Waterfall

Below is a scenario analysis to illustrate a bps waterfall comparison between wire transfers and stablecoins.

Scenario A

High-liquidity and adoption markets for stablecoins are characterized by deep on/off ramps through exchanges, OTC desks. They are fueled by strong demand drivers like remittances, inflation, or FX shortages, making stablecoins a practical dollar substitute for households and SMEs. While regulation often sits in a gray zone, usage is tolerated and widespread, with retail, freelancers, and merchants regularly transacting in stablecoins. Liquidity tends to concentrate on specific chains (e.g., USDT on Tron, USDC on Ethereum), allowing for cheap, fast, large-scale settlement across these corridors.

In high liquidity receiving corridors (USD-EUR, USD-GBP, USD-JPY), stablecoins have minimal hops and FX spreads and can compete on total costs. They may not incur swap and bridge costs. If the adoption is high on the receiving side, the receiver may prefer to continue holding and spending the money in the form of stablecoins without incurring off-ramp and local payout fees. If the adoption is high on the sending side, per-transaction gas fees come down furthermore.

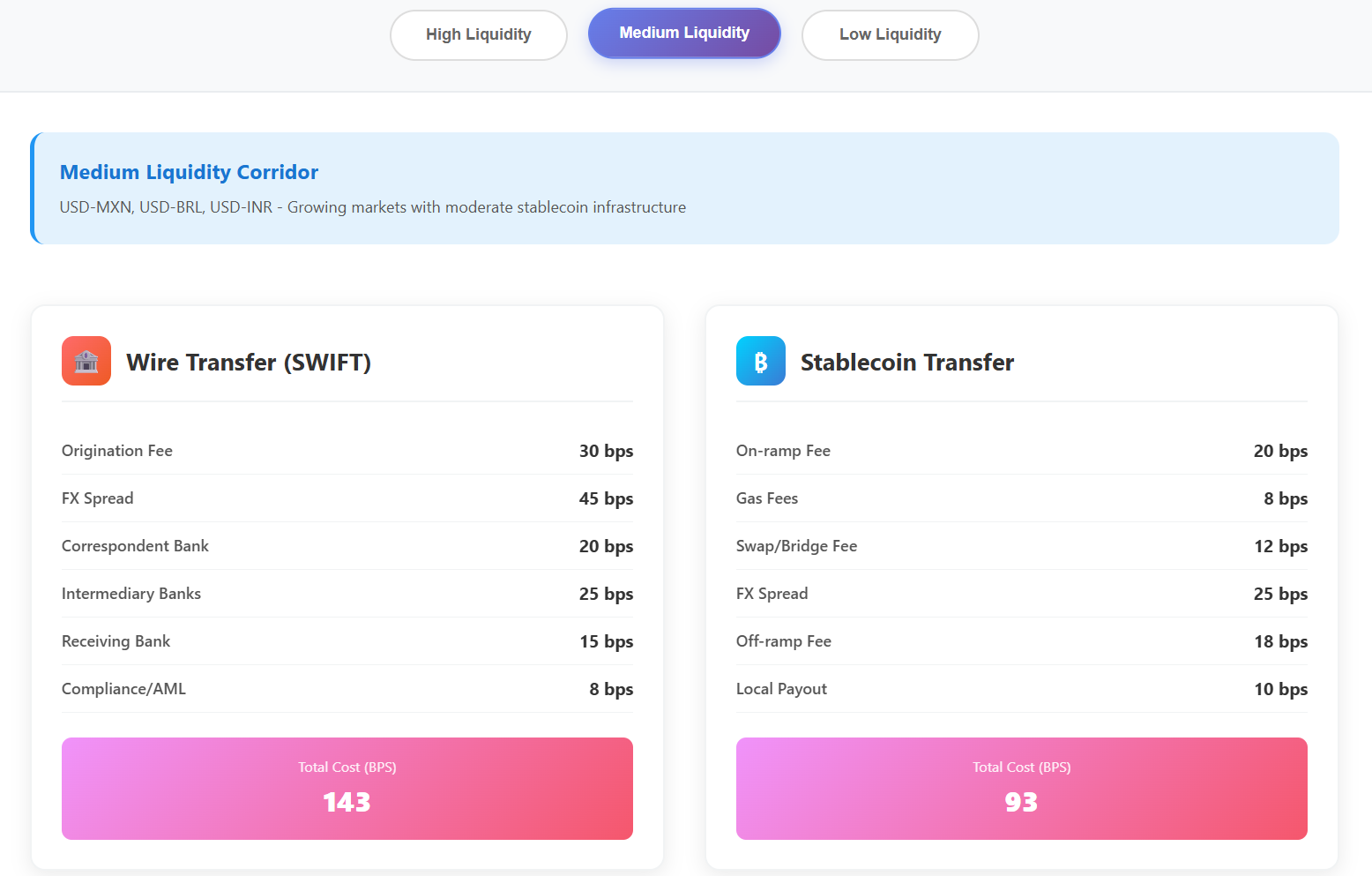

Scenario B

A medium liquidity market is one where stablecoins are known and available but not deeply entrenched in day-to-day transactions. Liquidity exists but spreads are wider vs. high-liquidity markets. Adoption often sits in specific verticals (remittances, freelancers, crypto trading) rather than being economy wide. Regulatory stance is uncertain or cautiously permissive.

In medium liquidity corridors (USD-MXN, USD-BRL, USD-INR), advantages are mixed. Stablecoins offer speed benefits, but wires may win on FX spreads. Local banking partnerships for stablecoin off-ramps become critical differentiators. Swap and bridge fees may apply when different stablecoins dominate the receiving market.

For Scenario B deployment, selective rail choice based on customer segments can work. Speed-sensitive customers justify stablecoin investment, while cost-sensitive customers prefer optimized wire solutions. Success requires tight cost control and strategic rail switching to manage margins.

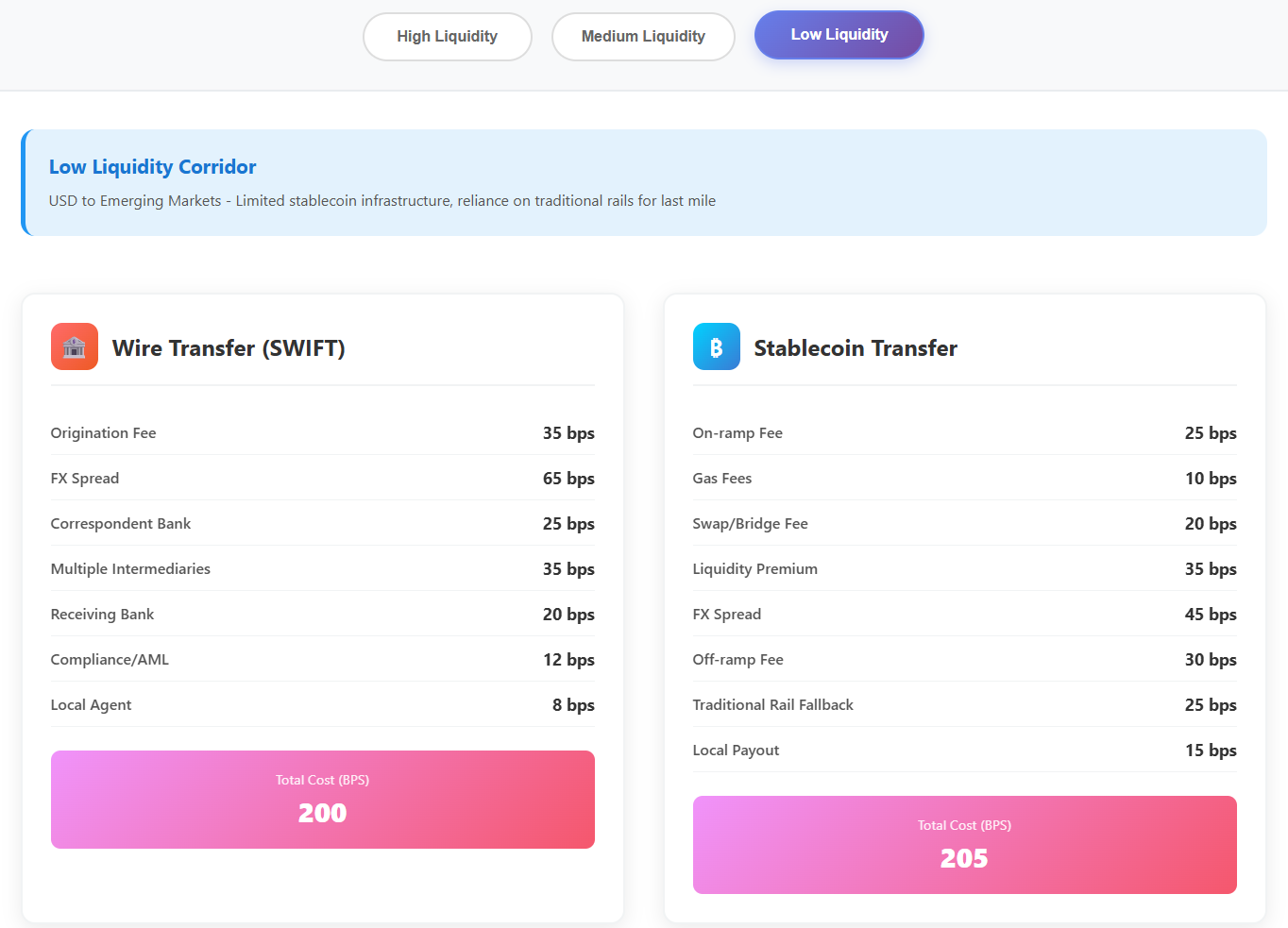

Scenario C

A low liquidity market has regulatory headwinds (ban/restriction), weak ramps (few exchanges, poor FX liquidity), thin demand drivers (no remittance/gig/commerce push), high spreads and poor usability, and absence of corporate adoption.

In low liquidity corridors (USD to emerging markets), wire advantages dominate through established correspondent relationships and regulatory clarity. Banks have decades of compliance frameworks and operational procedures for traditional rails. Stablecoins have limited local infrastructure, forcing last-mile payouts to fall back on traditional rails. This makes stablecoin transactions costlier than wires. Off-ramp liquidity constraints create settlement delays that eliminate speed advantages.

These are wait-and-watch scenarios. A wire-first approach with selective stablecoin pilots offers a path forward. This requires continuous monitoring for regulatory clarity and local partnership opportunities.

Approaches for Orchestrators

The fundamental difference with volume increases is that Wire costs scale with intermediary margins, Stablecoin costs scale with infrastructure efficiency. Adding stablecoins without cannibalizing wire revenue requires careful sequencing and customer segmentation. Here are a few approaches adopted by successful orchestrators.

Selective Introduction

Target high-liquidity corridors where stablecoin cost advantages are most pronounced. USD-EUR and USD-GBP transactions offer clear value propositions for customer pilots. Start with tech-forward customers who value innovation and speed over lowest-cost execution. These early adopters provide feedback while minimizing revenue risk from traditional customer segments. Leading fintech orchestrators are adopting this approach, selectively introducing stablecoin capabilities for specific use cases while maintaining traditional rails for standard operations.

Volume Capture

Once you have selected your send and receive corridors, volume capture is the key. Higher volumes bring in unit economics. Orchestrators can offer competitive pricing through dynamic models that reflect actual cost structures and by leveraging lower stablecoin processing costs. Better pricing drives transaction volume growth and creates cross-sell opportunities along-side traditional rails. Operational excellence investments ensure reliable service delivery and scalability of compliance frameworks, risk management protocols, and customer support capabilities. Wise exemplifies this strategy, achieving 41% underlying income CAGR by systematically reinvesting operational efficiencies into lower customer pricing and enhanced service capabilities.

Portfolio Optimization

Once you have volume flowing, it is time for optimization. Data-driven routing algorithms optimize rail selection by customer, corridor, and transaction characteristics. Smart routing considers cost, speed, reliability, and customer preferences simultaneously. Gains from optimization can extend value proposition beyond basic money movement and create additional revenue streams (FX hedging, cash flow financing, and treasury services) and partnership ecosystems. This can be invested back into scaling infrastructure, processing capabilities, compliance systems, and customer service to handle 3-5x transaction growth without proportional cost increases.

J.P. Morgan's approach with JPM Coin's programmable payment features driving expanded product adoption and cross-selling opportunities across their corporate client base is a good example for this approach.

Competitive Moat Development

Finally, strategize to build a strong competitive moat. Riding only on cost and speed as value drivers can only take you so far. Invest in creating platform and ecosystem integration depth. APIs, workflow automation, and data dependencies create friction for competitors attempting customer acquisition. Infrastructure sharing and white label stablecoin payment solutions generate additional revenue streams and can expand network effects. Anonymized payment flow analytics provide valuable insights to fintech partners, regulatory bodies, and market research firms and help trust and educate users. Every piece of infrastructure investment can create a stickiness that contributes to customer retention.

To conclude, the future of cross-border payments is not about choosing between traditional and digital rails but mastering strategic orchestration. As stablecoin infrastructure matures and regulatory frameworks crystallize, payment orchestrators who develop sophisticated routing capabilities, maintain cost discipline, and build deep customer integration will capture disproportionate value. The winners will be those who turn the complexity of multi-rail management into a sustainable competitive advantage.

Was this article helpful?